Buying your first home ranks among life’s biggest financial decisions. The median home price hit $420,800 in 2024, making preparation more important than ever.

We at Home Owners Association compiled essential tips when buying your first home to guide you through this complex process. Smart planning prevents costly mistakes that drain your savings.

Calculate Your True Budget and Affordability

Determine Your Maximum Housing Payment

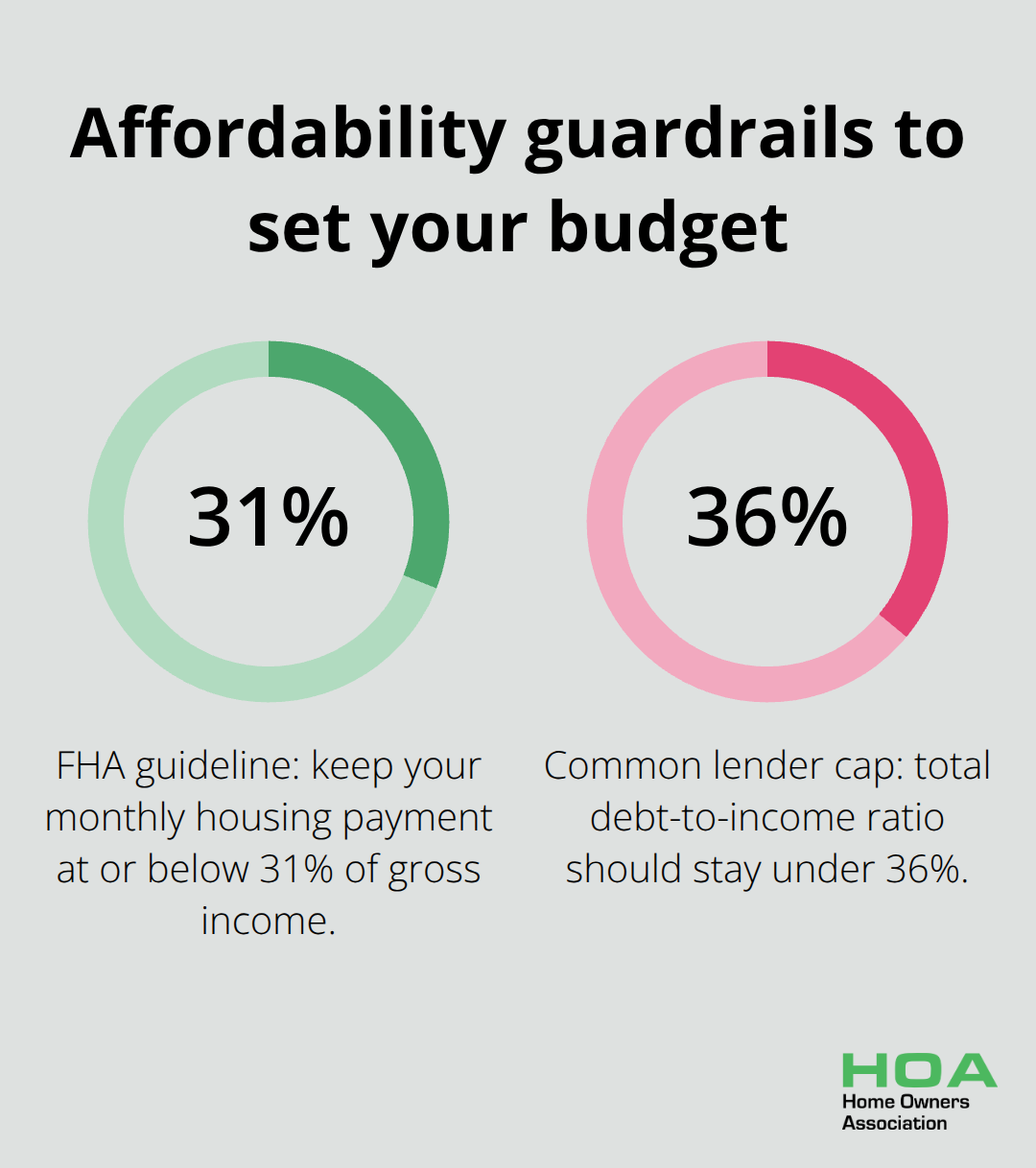

Your monthly housing payment should never exceed 31% of your gross monthly income according to the Federal Housing Administration guidelines. This means if you earn $5,000 monthly, your maximum housing payment caps at $1,550. Most lenders use the debt-to-income ratio of 36%, which includes all monthly debt payments.

Calculate your true affordability by subtracting existing debts like car loans and credit cards from this 36% threshold. The National Association of Realtors reports that 88% of buyers underestimate their total monthly housing costs by failing to include property taxes, insurance, and maintenance.

Build Your Down Payment Strategy

Traditional advice pushes 20% down payments, but most first-time buyers put down less than 10%. Save aggressively for at least 5% to access most loan programs (though you’ll pay Private Mortgage Insurance until reaching 20% equity).

Open a high-yield savings account dedicated solely to your home fund and automate transfers immediately after each paycheque. The First Home Super Saver Scheme in Australia allows saving up to $50,000 through superannuation with tax advantages.

Optimise Your Credit Score

Your credit score directly impacts your mortgage rate and costs thousands over the loan term. A 760+ score qualifies for the best rates, while scores below 620 face significantly higher costs or loan denials. Pay down credit card balances to below 30% utilisation immediately, and avoid opening new accounts during your home search.

Experian data shows that paying off collections accounts can boost scores by 20-40 points within 30 days (making this your fastest improvement strategy). These financial preparations set the foundation for the next critical step: securing mortgage pre-approval to strengthen your position in competitive markets.

Essential Steps in the Home Buying Process

Secure Your Mortgage Pre-Approval First

Pre-approval gives you serious buyer status and reveals your exact purchasing power before house hunting begins. Banks typically complete pre-approval within 24-48 hours and the letter remains valid for 60-90 days. Pre-approved buyers have significant advantages in the closing process because sellers prioritise offers from verified buyers.

Submit recent pay stubs, tax returns, and bank statements to expedite the process. Your pre-approval amount becomes your non-negotiable ceiling regardless of how perfect a property seems.

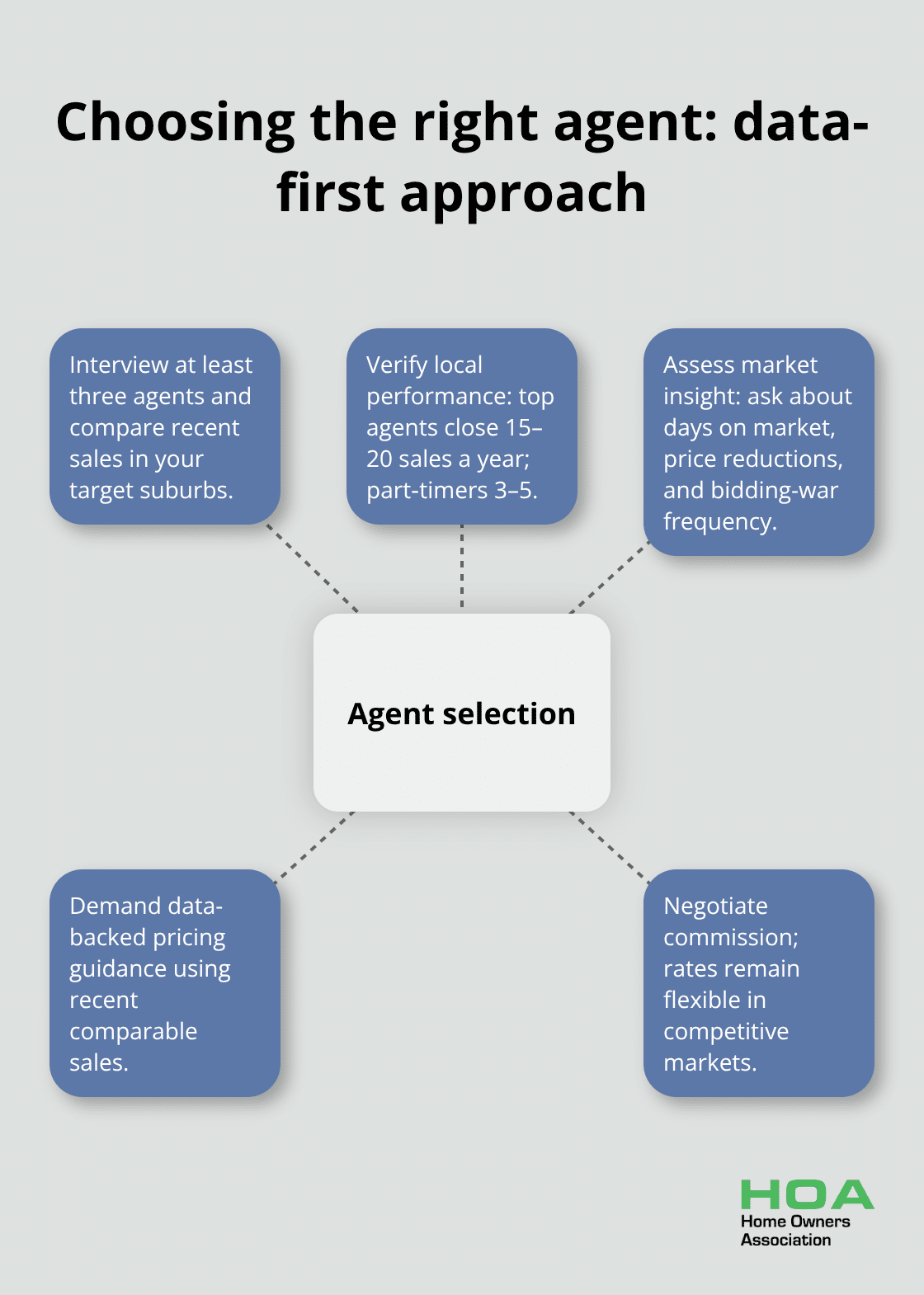

Choose Your Agent Based on Local Market Data

Real estate agents earn commissions only when transactions close, which creates natural alignment with your success. Interview three agents minimum and demand recent sales data from your target neighbourhoods. Top-performing agents close 15-20 transactions annually compared to part-timers who manage 3-5 deals.

Ask specific questions about average days on market, recent price reductions, and bidding war frequency in your price range. Commission rates stay negotiable despite industry standards (especially in competitive markets where multiple offers become common).

Research Neighbourhoods Through Multiple Data Sources

School ratings, crime statistics, and property tax rates impact both daily life and resale values significantly. Zillow reports that homes in top-rated school districts command 20% premiums over comparable properties in average districts.

Walk neighbourhoods at different times including weekends and evenings to observe traffic patterns, noise levels, and community activity. Check municipal websites for planned developments, road construction, or zoning changes that could affect property values. Recent sales comps within 0.5 miles provide the most accurate pricing benchmarks for your offers.

These preparation steps position you to make informed decisions when you begin property inspections (where hidden issues can derail even the most carefully planned purchases).

What to Look for During Property Inspections

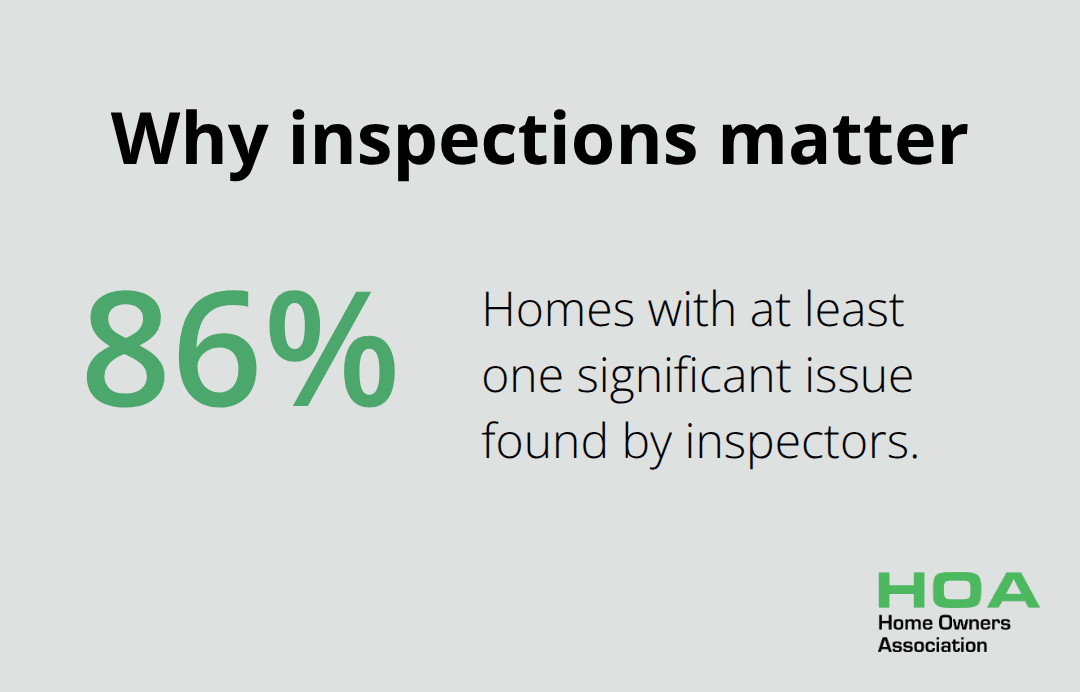

Professional inspections cost $300-800 but save thousands by catching major defects before you commit to purchase. The American Society of Home Inspectors found that 86% of homes have at least one significant issue that requires immediate attention or future repair.

Foundation and Structural Problems

Foundation problems top the most expensive discoveries, with repair costs that typically range from $2,200-8,100 with an average of $5,100 depending on severity. Check for cracks wider than 1/4 inch in basement walls, uneven floors that suggest settling, and water damage around the foundation perimeter. These issues signal serious structural concerns that affect the home’s stability and value.

Electrical and Plumbing Systems

Electrical systems built before 1980 often need complete rewiring at costs that exceed $8,000. Outdated plumbing with galvanised pipes requires replacement within 5-10 years. Modern electrical codes demand GFCI outlets in bathrooms and kitchens, while old wiring poses fire hazards that insurance companies flag during coverage reviews.

HVAC and Roofing Concerns

HVAC systems over 15 years old face replacement costs of $3,000-7,000, and roof repairs average $8,000 for asphalt shingles. Windows with broken seals or single-pane glass waste energy and need upgrades soon after purchase. These major systems impact both comfort and monthly utility bills significantly.

Pest and Hidden Damage Issues

Termite damage affects 600,000 homes annually according to the National Pest Management Association, with treatment and repairs that cost $3,000 on average. Smart buyers negotiate repair credits or walk away from properties with multiple major issues rather than absorb these unexpected expenses. Schedule inspections within your contract’s inspection period and use findings to renegotiate price or request seller repairs before you finalise the purchase.

Final Thoughts

These tips when buying your first home create your roadmap to successful homeownership. Smart buyers stick to their pre-approved budget limits, complete thorough inspections, and avoid emotional decisions that lead to overpaying. The biggest mistake involves skipping professional inspections to save a few hundred dollars (which often costs thousands in hidden repairs later).

Never waive contingencies in competitive markets without understanding the risks. Buyers who rush decisions frequently overlook neighbourhood research and end up in areas that don’t match their lifestyle needs. Missing pre-approval steps weakens your negotiating position against cash buyers.

After you make your purchase decision, focus on building relationships with reliable contractors and service providers. We at Home Owners Association help Melbourne homeowners access expert guidance for renovation projects. Property ownership brings ongoing responsibilities, but proper preparation makes the journey rewarding rather than overwhelming.